You own less of your company than you think you do.

Not because anyone tricked you. Dilution doesn’t happen in one dramatic moment. It happens in five separate “reasonable” decisions that each looked fine on their own. A 20% seed round here. A 10% option pool refresh there. A 25% Series A. Each one felt manageable. Add them up, and you’re suddenly a minority shareholder in the company you built.

Here’s the uncomfortable part: the advice to “just focus on growing the pie, not your slice of it” is true exactly once. After that, the governance terms buried in your term sheet, not the valuation headline, decide who’s actually running the company.

This is the guide to making sure that’s still you.

What Actually Determines Who Controls Your Company?

Cap table management uses simple arithmetic. Cap table outcomes are not, because they compound, and because most founders read the number (valuation, ownership %) and skip the paragraph (board composition, protective provisions, anti-dilution clauses).

Here’s the inside-circle term worth knowing: decision rights. In plain English: this just means who actually gets the final call on hiring, budget, and strategy after the round closes. A founder can hold 55% ownership and still lose decision rights if the term sheet hands the board a veto on key votes. The number on the cap table and the authority in the room are two different negotiations. Most founders only negotiate one of them.

How Much Startup Dilution Is Normal At Each Funding Stage?

$0–$100K: This is the founder/co-founder split conversation. Put the startup dilution rates in writing with a vesting schedule (standard: 4 years, 1-year cliff) before it becomes an emotional conversation instead of a structural one. Think of it as a founder prenup: awkward to set up, but far more awkward to negotiate after a relationship sours. The same operational discipline that makes your first client relationship work, clear terms, written agreements, and no ambiguity applies just as much to your first equity split.

$100K–$1M: Your first SAFE or priced round. This is where the pre-money vs. post-money confusion costs founders real percentage points, covered in detail below.

$1M–$5M: Series A. Dilution cascades here: the SAFE conversion, the option pool top-up, the new investor’s stake, all landing in the same round. This is where founders are most likely to be surprised by their post-round number.

$5M–$10M: Cumulative dilution across three-plus rounds. Your pricing power (plain English: how much leverage you still have to say no to bad terms) shrinks with every round unless you’ve been protecting it deliberately. This is also where cap table discipline and cash flow discipline start to intersect: a founder juggling tight payment terms has less runway, and less runway means less leverage in the next negotiation.

Cap Table Management: The Lateral Pivot

The common advice is “get the biggest valuation you can.” That’s the wrong optimization target. Valuation is the least durable number in the term sheet: it changes every round anyway. What doesn’t reset is the governance structure you agree to.

Valuation resets every round. Governance doesn’t.

The wedge: before your next round, write a one-page “dilution rationale,” not for investors, for yourself. Tie every percentage point you’re willing to give up to a specific milestone that capital unlocks. If you can’t explain why you’re giving up 20% instead of 15%, you’re not negotiating a number. You’re accepting one.

What’s the Five-Step Way to Protect Your Cap Table?

- Build one single source of truth. Not a spreadsheet you reconstruct every fundraising cycle. A live, always-current cap table. Tools like Carta or Pulley exist for exactly this. If you can’t answer “what does everyone own right now” same-day, you don’t have a cap table. You have a rumor.

- Audit every instrument. Line by line: every SAFE, every convertible note, every side letter, cross-referenced against signed documents. This is the boring work that prevents the expensive surprise: a buried anti-dilution clause or a double-counted SAFE that blows up a term sheet mid-negotiation.

- Model two rounds forward. Not just this raise. The next one too. A dilution that looks fine in isolation can be brutal once you stack it against what’s coming.

- Split the negotiation. Treat valuation and governance as two separate conversations. Bend on price if you need to. Hold the line on board seats and protective provisions. That’s where real control lives.

- Question the “market standard.” When a term is labeled standard, ask what specific problem it solves for the investor. Most boilerplate is a starting offer, not a law of physics.

Which Cap Table Management Mistakes Cost Founders the Most Equity?

- Pre-money vs. post-money confusion. A $1M investment at a $4M pre-money valuation gives investors 20%, not 25%. Get this backwards and you’ll misjudge every round that follows.

- Treating rounds in isolation. A “manageable” 20%, then 18%, then 15% compounds into owning less than half your own company, and it happens faster than most founders expect.

- Skimming governance clauses. The valuation is the headline. Anti-dilution provisions, liquidation preferences, and board composition are the fine print that actually determines who’s in charge when things get hard.

- Post-money SAFEs stacked carelessly. These shift all the dilution risk onto founders instead of splitting it with future investors. Multiple SAFEs at different valuation caps, unmodeled, is how founders wake up owning far less than they thought.

Would I Fire Someone For This?

The question of whether to fire an employee or not should be seen as a gut-check instead of a guilt trip:

- Would I fire a CFO who couldn’t produce an accurate cap table same-day? → If you can’t either, that’s step one, today.

- Would I fire an ops lead who signed a vendor contract without reading the liability clause? → Same standard applies to your own term sheet.

- Would I fire someone who accepted “market standard” terms without asking what they cost us? → Then don’t do it yourself.

- Would I fire someone who didn’t model the next two rounds before committing to this one? → Model it before you sign, not after.

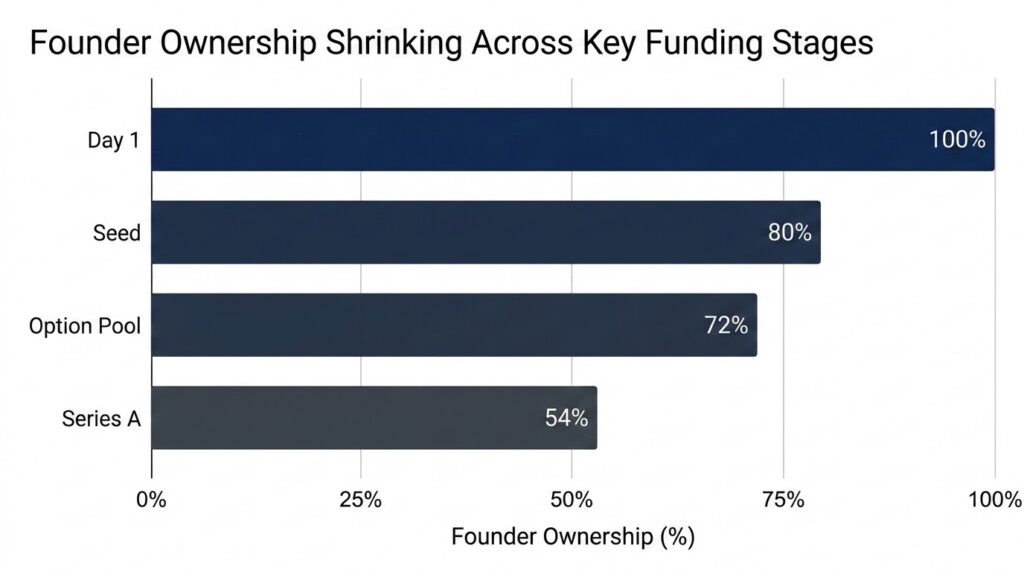

The Real Numbers

Simplified for illustration. Run your actual numbers through a cap table tool before making decisions.

Assumptions: Founder starts with 100% ownership.

| Event | Founder Ownership |

|---|---|

| Day 1 | 100% |

| After $1M seed round ($5M post-money SAFE cap → investor takes 20%) | 80% |

| After 10% option pool created pre-Series A | ~72% |

| After $8M Series A ($32M post-money → new investor takes 25%) | ~54% |

Each individual round looked reasonable: 20%, then a routine pool top-up, then 25%. Two priced rounds and one pool refresh dropped this founder from full ownership to just over half.

What breaks the math further: additional option pool refreshes at Series B, pro-rata rights letting early investors keep re-buying their percentage in every future round, multiple SAFEs stacked at different valuation caps, or a down round triggering anti-dilution ratchets that protect investors at the founder’s direct expense.

What To Do Next

- 24 hours: Pull your actual cap table (the real one, not the one in your head) and check who owns what today.

- 7 days: Run every SAFE, note, and side letter through a line-by-line audit against signed documents.

- 30 days: Build a two-round-forward dilution model before you take a single investor meeting for your next raise.